Minimum Alternate Tax Mat Pdf

Minimum Alternate Tax

Minimum Alternate Tax Tax Credit Tax Deduction

Mat Vs Amt Minimum Alternate Tax And Alternative Minimum Tax Vakilsearch

Title Minimum Alternate Tax Mat Author Ca Kamal Garg Publisher Bharat Law House 6th Edition 2017 Type Paperback Vorabookh Vora Books Bookstore

Minimum Alternate Tax In India A Comparative Analysis Of Provisions Under Income Tax Act And Direct Tax Code

Guide To Minimum Alternate Tax For Ind As Compliant Companies

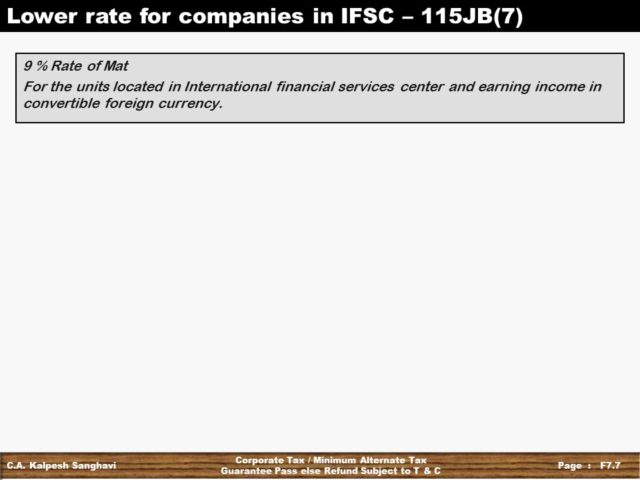

In the case of a non corporate taxpayer to whom the provisions of alternate minimum tax amt applies tax payable cannot be less than 18 5 hec of adjusted total income computed as per section 115jc.

Minimum alternate tax mat pdf.

All About Alternate Minimum Tax Amt Section 115jc

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Https Papers Ssrn Com Sol3 Delivery Cfm Ssrn Id1759907 Code1612178 Pdf Abstractid 1759907 Mirid 1

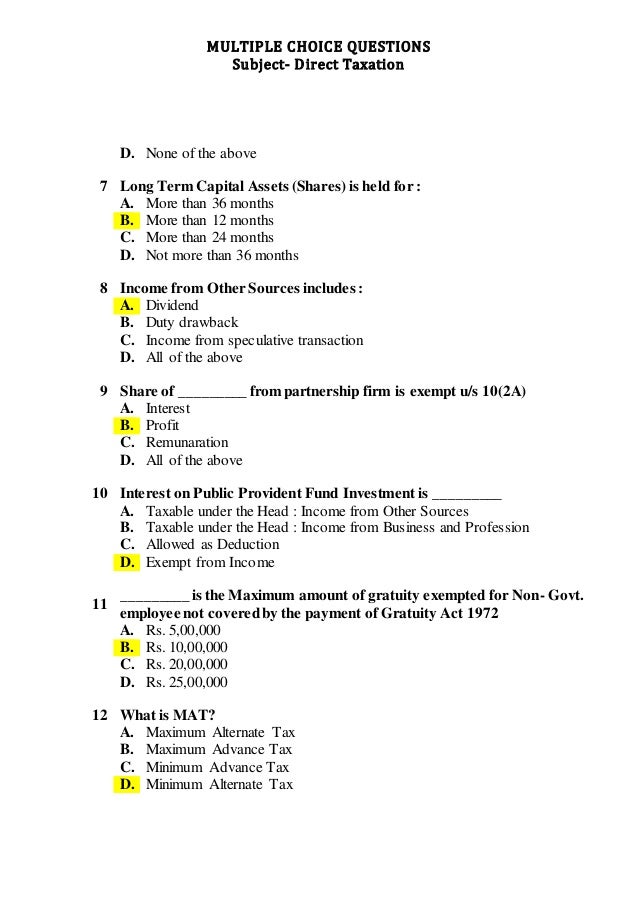

Ca Final Question Bank Dt Minimum Alternate Tax Mat

Source : pinterest.com