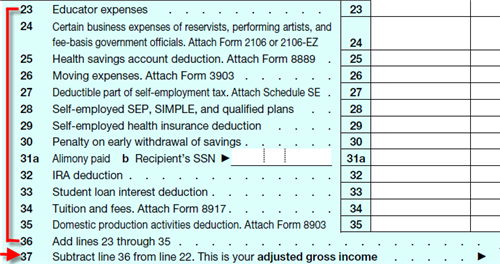

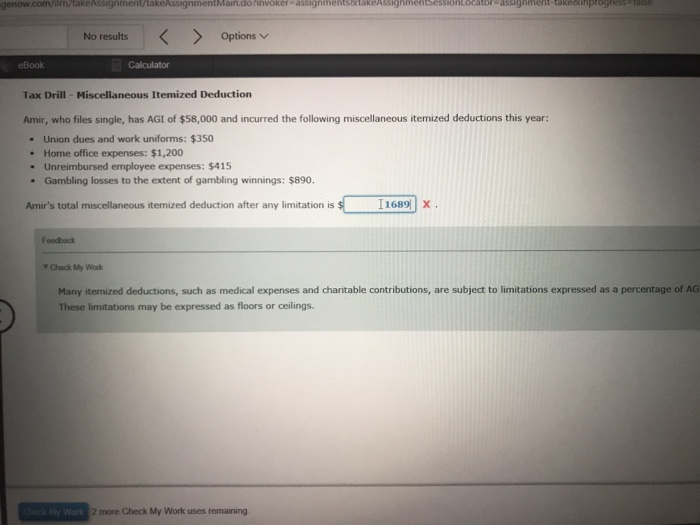

Miscellaneous Itemized Deductions Floor

The Ultimate List Of Itemized Deductions Standard Deduction Deduction Tax Deductions List

Tax Deductions Above The Line Standard Itemized And Miscellaneous

It Is Such A Shame To Work All Year Find Out You Have Money Coming Back And Th Tax Day Tax Forms Tax Time

It S Your Favorite Post Of The Week Time To Test Your Knowledge With An Mcq Leave A Comment With Your Answer And We Ll Let Yaeger Cpa Review Blog Cpa R

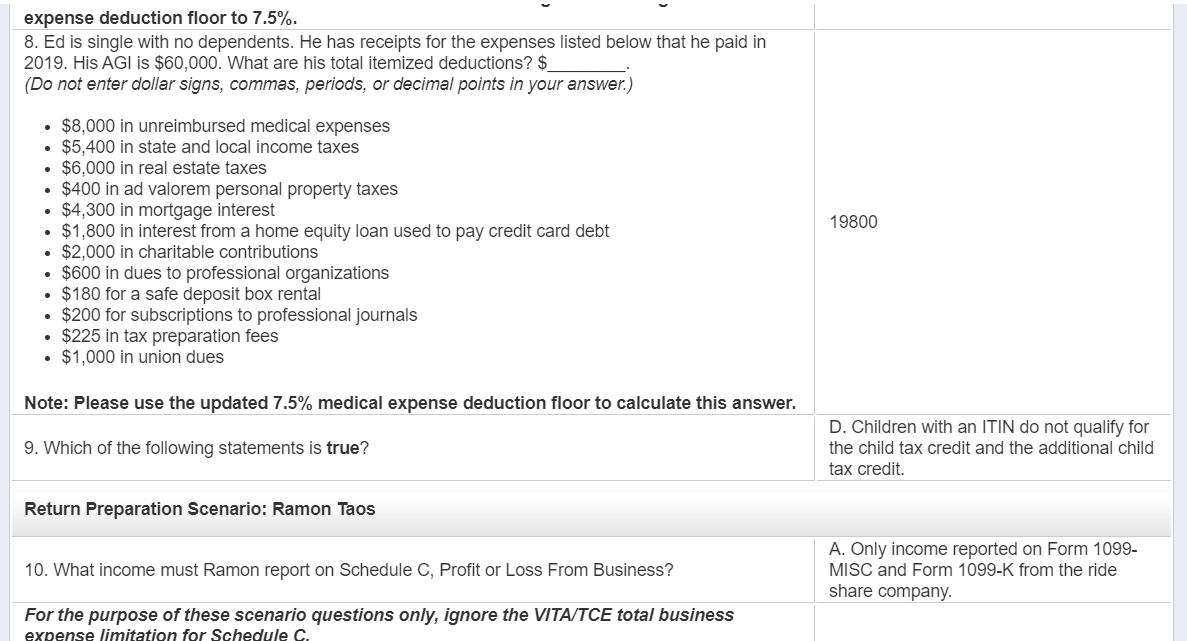

Expense Deduction Floor To 7 5 8 Ed Is Single W Chegg Com

Tax Reform 2018 The Impact On Itemized Deductions For Individuals Jfs Wealth Advisors

Starting on january 1 2018 and running through december 31 2026 individuals will no longer have the ability to deduct the excess expenses listed below as itemized deductions on their 1040s.

Miscellaneous itemized deductions floor.

Known Facts About Direct Admission In Top Mba College University Of Delhi College Names Mba

Keep Your Agency Profitable And Compliant With The Coding Institute S Post Acute Newsletters To Avail Additional 20 O Medical Coding Post Acute Care Coding

6980905 The European Union Reform Company

Investment Fees Are Not Deductible But Borrow Fees Are Investing Best Term Life Insurance Life Insurance Companies

Source : pinterest.com